The Problem with Doing Everything Right

This is a short reflection on Clayton Christensen’s The Innovator’s Dilemma, focusing on the introduction and its central argument about why strong, well-managed companies can still lose their position when technologies shift.

CORPORATE ENTREPRENEURSHIP

E.J. Hofmann

4/6/20264 min read

Reflection

What makes Christensen’s introduction so compelling is that it does not begin with the comforting assumption that companies fail because they are lazy, stupid, or badly run. In fact, he argues almost the opposite. The real problem is harder to accept: firms often fail precisely because they are doing what good management is supposed to do. They listen to customers, track margins, invest where returns are visible, and allocate resources toward the most promising mainstream opportunities. That is exactly what makes the argument unsettling. Failure, in this account, is not usually the result of managerial negligence. It is built into the logic of success itself.

The introduction makes this point through a series of examples that are meant to feel counterintuitive. Sears, Digital Equipment Corporation, IBM, Xerox, and major steel firms were not fringe cases or obviously incompetent organizations. They were, at one stage, admired leaders. Christensen’s claim is that the very processes that helped them dominate existing markets also made them less capable of responding to disruptive change. That distinction between sustaining and disruptive technologies is the conceptual core of the introduction. Sustaining technologies improve what established customers already value. Disruptive technologies begin by underperforming on those familiar measures, but they introduce a different package of benefits: lower cost, simplicity, convenience, or accessibility. Established firms tend to dismiss them because, viewed through current customer demand and financial metrics, they do not initially look attractive.

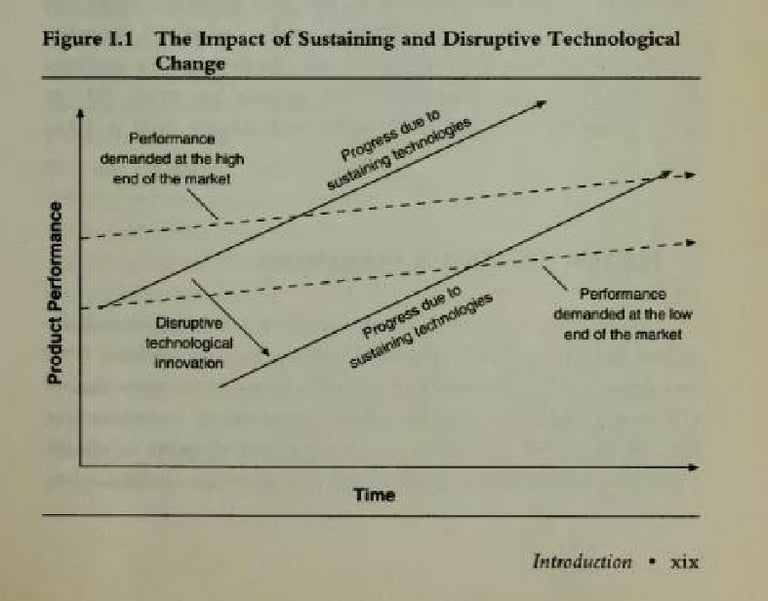

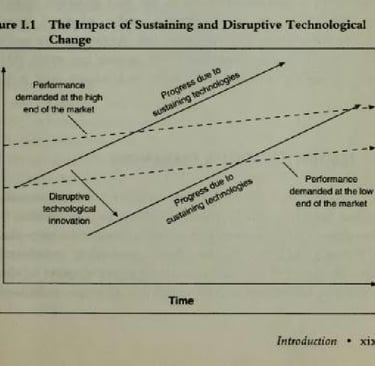

That is the most interesting insight here: disruption is not just a technological event. It is also a perceptual and organizational problem. On page xix, the graph labeled “The Impact of Sustaining and Disruptive Technological Change” visually sharpens the point. Sustaining innovation climbs faster and faster up the performance trajectory, while disruptive innovation enters below the mainstream market’s expectations. But the market itself does not stand still. Needs at the low end and high end shift differently, and firms can end up overshooting what many customers actually require. In other words, companies can improve themselves into vulnerability. That is a powerful idea because it turns the standard story of progress upside down. More innovation is not always strategic wisdom; sometimes it is a way of becoming increasingly well-adapted to the wrong game.

More specifically, Christensen is questioning one of management’s quiet assumptions: that better data and closer alignment with present customers will naturally produce long-term success. His answer is no. Present customers are often poor guides to future markets, especially when new technologies first appear crude, niche, or commercially minor. Rational investment, then, can become a trap. Managers are not misreading the evidence in front of them; they are reading the wrong horizon.

The deeper question the introduction leaves me with is whether disruption is really about technology at all, or whether it is more fundamentally about institutional attention. Who gets listened to? Which markets count as real? Which forms of value are taken seriously before they become profitable? Christensen seems to suggest that firms fail not because they cannot innovate, but because they cannot justify, inside their existing logic, the kind of innovation that would save them. That is a sharper and more durable argument than the familiar cliché that companies simply “resist change.” Often, they do not resist change. They manage it well. Just not the change that matters most.

Source: Christensen, “The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail”,(introduction only), Boston: Harvard Business School Press

Q&A

1. What is the “Innovator’s dilemma” exactly?

The innovator’s dilemma is the paradox that well-managed, successful firms can fail because they follow the logic that usually makes them successful. Christensen’s point is not that these firms are incompetent. It is that they listen to their customers, invest in improvements those customers want, and put resources into markets that promise the strongest returns. Under normal conditions, that is good management. But when a disruptive technology appears, those same habits can push firms away from the very innovations that later reshape the market.

So the dilemma is this: companies are rewarded for prioritizing existing customers and profitable sustaining improvements, yet that very rational behavior makes it difficult for them to invest in early-stage disruptive technologies that initially look worse, smaller, and less profitable. In other words, firms often fail not in spite of good management, but because of it.

2. How is the disruptive vs. sustaining distinction different from the radical vs. incremental distinction?

This is an important distinction. Christensen is not mainly sorting technologies by how big or dramatic the technical change is. He is sorting them by how they relate to the market and to customer demand. Sustaining technologies improve product performance along dimensions mainstream customers already value. Disruptive technologies, by contrast, may initially perform worse on those mainstream measures, but they introduce a different kind of value: they are often cheaper, simpler, smaller, or more convenient.

That is why disruptive does not simply mean radical, and sustaining does not simply mean incremental. A technology could be technically radical and still be sustaining if it helps established firms serve their main customers better. Likewise, a disruptive technology may not look technically impressive at first; what makes it disruptive is that it changes the basis of competition and opens space in overlooked or emerging markets. Christensen is shifting the question from “How novel is the technology?” to “What kind of market path does it create?”

3. Why do firms not invest in disruptive technologies?

Firms do not invest in disruptive technologies because, at first, those technologies make very little sense inside the firm’s existing decision framework. Christensen gives three linked reasons. First, disruptive technologies usually promise lower margins, not higher ones. Second, they tend to emerge in small or insignificant markets, which are not attractive to large firms that need sizeable returns. Third, the earliest versions often do not satisfy the needs of a company’s best customers, so there is little pressure from mainstream demand to pursue them.

In practice, that means managers are not ignoring disruption out of laziness. They are making what look like disciplined, rational choices. Their customers are asking for better versions of existing products, their financial systems reward larger and safer markets, and the disruptive option appears commercially weak. The problem is that by the time the disruptive technology improves enough to matter to the mainstream, it is often too late. That is why the dilemma is so difficult: the evidence inside the firm tells managers not to invest—until the market has already moved.

© 2025. All rights reserved.

Espen Hofmann

B.Sc. in Human Resource Studies: People Management (Tilburg University)

A personal archive of projects, research, tools, and ideas in progress.

This website is intended for informational purposes only.

The content is based on research, academic sources, and personal analysis.

Nothing here should be considered financial, legal, or investment advice.