Darwin and the Demon: Innovating Within Established Enterprise

by Geoffrey A. Moor

CORPORATE ENTREPRENEURSHIP

E.J. Hofmann

4/19/20268 min read

Innovation is one of those words that gets treated like a universal good. More innovation. Faster innovation. Constant innovation. It sounds obvious, almost moral. But Geoffrey Moore’s Darwin and the Demon makes a sharper point: the real issue is not whether a company innovates, but what kind of innovation it pursues, and when.

That distinction matters more than most leaders admit.

A company can be full of talent, serious about growth, and genuinely committed to change, and still back the wrong kind of innovation for the moment it is in. It can pour resources into product upgrades when the real opportunity is operational. It can chase breakthrough ideas when the smarter move is business model reinvention. It can keep celebrating the capabilities that made it successful long after those capabilities stopped mattering to customers. That is where Moore is strongest. He strips away the vague mythology around innovation and replaces it with something far more useful: context.

The mistake companies keep making

Most firms do not fail because they stop caring. They fail because they keep solving yesterday’s problem.

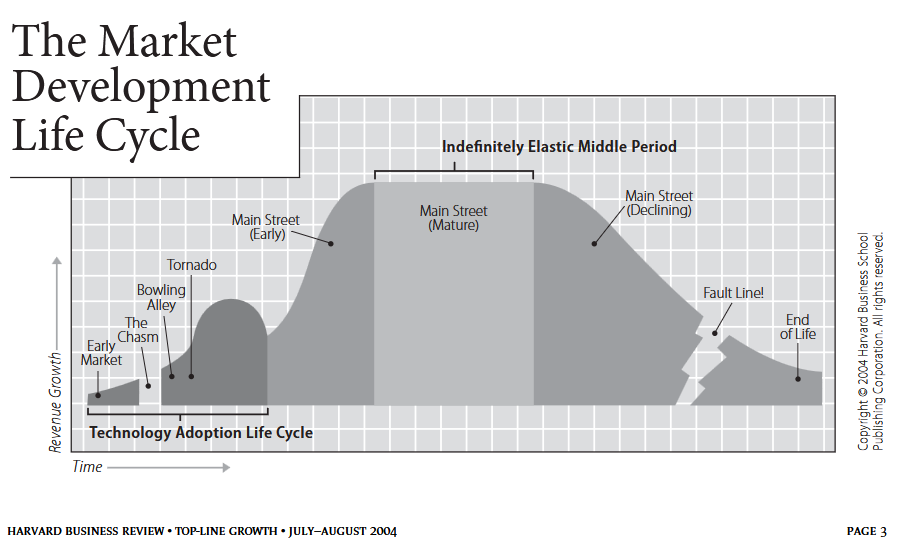

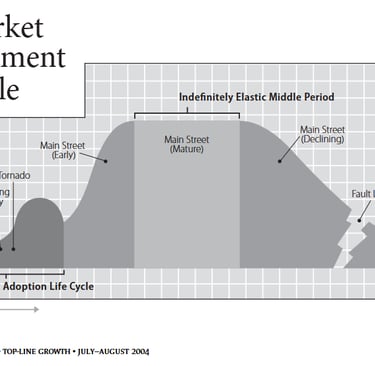

Moore’s framework starts from a simple but powerful premise: markets move through a life cycle, and different forms of innovation create value at different stages of that cycle. In the early phases, disruptive, application, and product innovation matter most because the market itself is still being formed. Later, once the category becomes established, those same forms lose leverage, and process, experiential, and marketing innovation become more important. Later still, as the market matures or declines, the real strategic work shifts again toward business model and structural innovation.

This is the part leaders often resist, because it cuts against corporate instinct. If a company became successful through product excellence, it wants to believe product excellence will keep carrying the day. If engineering built the franchise, the culture keeps deferring to engineering. If a heroic go-to-market push once saved the business, the organization keeps looking for another heroic go-to-market push. But markets do not care about a company’s emotional attachment to its strengths. They reward relevance, not nostalgia. That is Moore’s Darwinian point, and it lands.

Innovation is not one thing

One reason the article still feels useful is that it refuses to flatten innovation into a single category. Moore lays out a broader taxonomy: disruptive, application, product, process, experiential, marketing, business model, and structural innovation.

That list matters because it corrects a bad habit in management thinking. Too many conversations about innovation are really just conversations about new products. New features. New technology. New launches. The glamorous stuff.

But in practice, some of the most consequential innovation is much less cinematic.

A company can transform its economics through process innovation. It can deepen customer loyalty through experiential innovation. It can unlock growth by changing how it reaches customers, prices value, or positions itself in the value chain. These moves are often less romantic than “the next big thing,” but in an established market they may be far more valuable. Moore’s point is not that breakthrough innovation does not matter. It is that breakthrough innovation is not the only game in town, and often not the right one.

That is an important correction, especially in business cultures that equate seriousness with disruption. Not every company needs to invent the future from scratch. Sometimes it needs to remove friction, redesign incentives, or rebuild the way value is delivered. Those are not consolation prizes. They are strategy.

The life cycle is the strategy

To understand Moore’s argument, you have to take the life cycle model seriously.

He maps market development from the early market, through the chasm, bowling alley, and tornado, into several versions of Main Street, then finally into decline, fault line, and end of life. The visual model in the article makes the point clearly: markets do not stay in one condition, and innovation logic cannot stay fixed either. What works in the tornado will not work in mature Main Street. What works in early adoption will not rescue a category approaching obsolescence.

This is where the article becomes more than a classification exercise. It becomes a warning.

The danger is not just that markets evolve. The danger is that organizations do not evolve with them. A company can keep investing in the forms of innovation that feel most familiar, even after the market has stopped paying for them. Moore argues that once a market reaches Main Street, earlier-stage innovation types lose economic leverage; the returns no longer justify the investment in the same way. At that point, companies need different muscles.

That sounds obvious once stated. It rarely is in practice.

Why inertia is the real enemy

The title’s “demon” is not competition. It is inertia.

That is the most memorable idea in the piece, and probably the most enduring one. Moore argues that success itself generates resistance to change. The deeper a firm moves into a market life cycle, and the more successful it has been, the stronger the tendency to fall back on old habits, old structures, and old definitions of competence. The very capabilities that once created advantage become anchors.

This is not just a structural problem. It is a human one.

People build careers around particular strengths. Departments defend relevance. Leaders trust the instincts that got them promoted. The organization learns to admire certain forms of excellence and ignore others. Over time, this creates a subtle but powerful bias: the company keeps trying to win in ways it already understands.

And that is exactly why inertia is so difficult to beat. It does not feel like laziness. It feels like discipline. It feels like staying focused. It feels like protecting what made the company great. That is what makes it dangerous.

Construction is not enough

More specifically, Moore is blunt about the usual corporate fantasy: leaders think they can build the new while leaving the old untouched.

They cannot.

He argues that real change requires both construction and deconstruction. Companies must create new innovation capacity, yes, but they must also aggressively pull resources out of legacy processes and organizations that no longer create differentiation. Otherwise the old system simply absorbs the energy of the new one.

That is a harder message than “launch an innovation initiative.” It means trade-offs. It means dismantling duplicative structures. It means standardizing processes that teams insist are special. It means deciding that some forms of variation are not strategic assets but expensive habits.

Moore’s prescription for legacy work is strikingly unsentimental: centralize it, standardize it, simplify it, then automate or outsource it. The governing principle is just as direct: productivity, not differentiation. If a process no longer shapes customer preference, stop treating it like a sacred expression of the firm’s uniqueness.

That is not glamorous advice. It is also the kind of advice companies usually need most.

Leadership has to shift too

One of the smartest details in the article is that Moore does not treat innovation leadership as fixed. He ties sponsorship and leadership to the type of innovation being pursued. Early-stage and company-shaping innovation need broader executive authority. Mid-cycle innovation can often sit lower in the organization. Late-stage reinvention requires CEO-level backing because it touches the structure and identity of the enterprise itself.

That matters because many companies misread innovation as a culture issue when it is really a governance issue.

They talk about creativity when the actual problem is sponsorship. They celebrate experimentation while starving the effort of institutional protection. Or they assign transformative work to teams with neither the power nor the legitimacy to challenge the legacy system. Then they act surprised when nothing moves.

In practice, innovation fails less often from lack of ideas than from lack of organizational permission.

What the article gets right, years later

The article was published in 2004, but its core logic still holds. In some ways, it feels even more relevant now.

Why? Because the pressure to innovate has intensified, while the ability to distinguish between types of innovation has not. Companies are surrounded by noise: AI, platform shifts, changing customer expectations, margin pressure, operational fragility, investor impatience. Under those conditions, there is a strong temptation to treat every strategic challenge as a call for breakthrough innovation.

But not every problem is solved by invention.

Sometimes the best move is better process design. Sometimes it is a simpler customer experience. Sometimes it is channel redesign, pricing redesign, or an entirely different business model. And sometimes the real challenge is not discovering the future but having the discipline to dismantle parts of the past.

That is where Moore remains useful. He brings innovation down from the level of slogan and puts it back into the world of timing, economics, and managerial judgment.

Conclusion: the real discipline is knowing what season you are in

Fundamentally, Darwin and the Demon is an essay about strategic maturity.

It asks a hard question: does your company actually understand the stage of the market it is in, or is it still behaving as if the old playbook applies? That question cuts deeper than most innovation talk because it forces a company to confront both external change and internal attachment. It is not enough to want innovation. You have to want the right innovation for the moment, and you have to be willing to take resources away from what no longer earns them.

That is the real tension Moore names. Darwin is the pressure of the market. The demon is the weight of institutional habit. One comes from outside. The other lives in the building.

And for established companies, the second threat is often the more dangerous one.

Comprehesion Q&A

What does “Darwin and the Demon” mean?

The title sets up the article’s two central forces.

“Darwin” refers to market evolution. Industries change, categories mature, products commoditize, and companies are forced to adapt or lose relevance. In Moore’s view, firms live inside a kind of economic natural selection: if they do not evolve their way of creating value, they get left behind.

“The demon” is inertia inside the company. It is the internal force that keeps organizations doing what used to work, even when the market has moved on. Moore’s point is that many firms are not defeated only by external competition or technological change. They are defeated by their own habits, structures, and attachment to legacy strengths.

So the title captures the tension perfectly: Darwin is the pressure to adapt; the demon is the resistance to adaptation.

Which type of innovation should firms focus on?

Moore’s answer is not “always disruptive innovation.” It depends on where the firm is in the market life cycle. That is the whole thesis of the article.

In the early stages of a market

Firms should focus mainly on:

Disruptive innovation

Application innovation

Product innovation

These matter in the early market, the chasm, the bowling alley, and the tornado because the category is still being created and validated. At that stage, the market rewards new offerings, new uses, and product advances.

Once the market reaches Main Street

The priority shifts toward:

Process innovation

Experiential innovation

Marketing innovation

Why? Because once a market is established, the earlier forms of innovation lose leverage. Customers no longer reward them in the same way, and the returns on those investments decline. At this point, companies create more value by improving efficiency, customer experience, and go-to-market effectiveness.

In mature or declining markets

Firms should increasingly look at:

Business model innovation

Structural innovation

These become critical when the category is commoditizing or nearing decline. At that point, the company may need to rethink how it creates value, where it sits in the value chain, or even how the enterprise itself is structured.

So the clean answer is this: firms should focus on the form of innovation that matches their market stage, not the form they are most comfortable with.

How can inertia be overcome?

Moore is very clear here: inertia is not overcome by simply adding a new initiative on top of the old organization. It has to be attacked directly.

1. Build the new

Companies need an innovation effort aimed at the next source of competitive advantage. Moore says this team should be backed by the right senior sponsor and led by someone with real expertise in the new innovation type being pursued. Often the leader should come from outside, while much of the team should come from inside the firm.

2. Dismantle the old

This is the harder half, and the part most companies avoid.

Moore argues that management must also deconstruct legacy processes and organizations. If leaders leave legacy structures untouched, the old system will continue absorbing resources and blocking change. The company must actively pull resources away from what no longer drives customer preference.

3. Follow the rule: productivity, not differentiation

For legacy work, Moore’s principle is simple: if a process no longer creates meaningful differentiation, stop treating it as special. The goal is not to preserve it elegantly. The goal is to make it more productive.

He recommends four steps:

Centralize the function

Standardize the process

Simplify the process

Automate or outsource the process

That sequence frees up resources that can then be redirected toward the newer, more relevant forms of innovation.

© 2025. All rights reserved.

Espen Hofmann

B.Sc. in Human Resource Studies: People Management (Tilburg University)

Research & Insights on Artificial Intelligence, Human Capital & the Future of Work

This website is intended for informational purposes only.

The content is based on research, academic sources, and personal analysis.

Nothing here should be considered financial, legal, or investment advice.

Impressum

Datenschutz